The energy sector has continued to perform well in 2023, from upstream production to midstream operators. Enterprise Products Partners L.P. (NYSE:EPD) has followed the trend as units have increased 7.56% YTD. EPD’s Q3 results were a bit of a mixed bag as they beat top-line estimates by $370 million, delivering $12 billion in revenue, but missed on EPS by $0.03 as they produced $0.60 per unit in Q3. Regarding midstream operators, I am less concerned about the bottom line number, as a portion is tied to fluctuating commodity pricing. I focus on the amount of distributable cash flow (DCF) that is being generated. The DCF is the most important metric to me because this is the pool of capital that midstream distributions are paid from, and the excess DCF, which is retained after distributions, is utilized to reinvest into the company. Recently, Exxon Mobil (XOM) agreed to acquire Pioneer Natural Resources (PXD), and Chevron (CVX) responded by agreeing to acquire Hess (HES) roughly 2 weeks later. I am more bullish on EPD today after learning that they plan on allocating $3.1 billion to develop 4 new capital projects to support growing production in the Permian Basin. I think EPD is still an attractive income investment as it has a 7.49% yield with 25 years of consecutive distribution increases. As the Fed begins to pivot, EPD could gain even more steam as the spread between their distribution yield and the yield from risk-free assets expands. EPD does issue a K-1 Tax Package, so please review this information or ask your tax professional about any K-1 questions you may have.

Seeking Alpha

The energy landscape and why the news about Enterprise Products Partner’s new capital projects is bullish for long-term investors

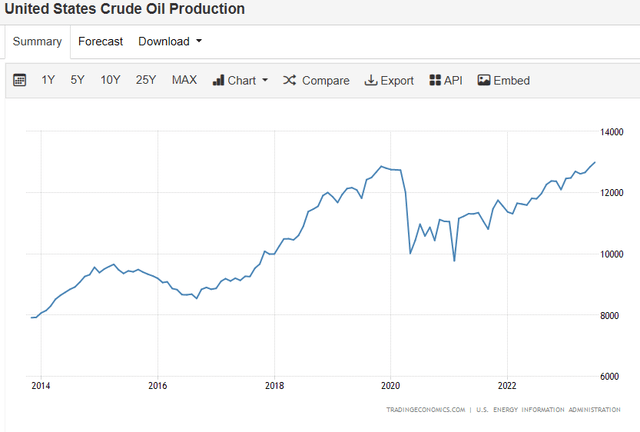

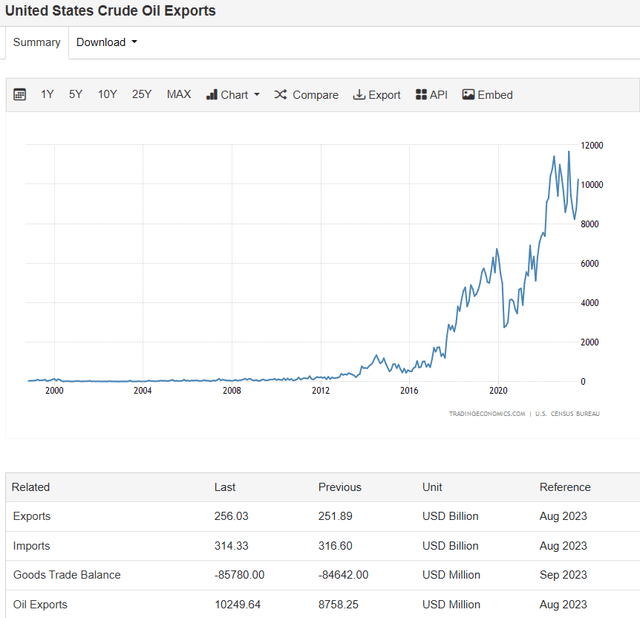

It could be me, but I feel as if the narrative regarding oil & gas is shifting. Back in 2020 and 2021, there was elevated talk pertaining to fossil fuel’s relevancy in the new world economy and that renewable energy was going to cannibalize traditional energy sources. In 2022, the unfortunate situation in Ukraine made everyone realize how dependent the world is on traditional energy sources. I hear fewer talking heads discussing how conventional energy sources will be a distant memory by 2040. The United States has continuously seen its oil producers ramp up production, and we are now producing the most barrels per day (bpd) in our nation’s history. The United States is also the largest oil and gas producer globally, and we are working our way back to being a net positive oil exporter.

Trading Economics Trading Economics

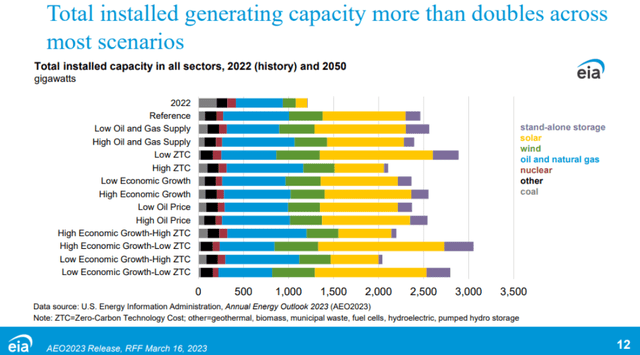

XOM just agreed to acquire PXD and stated that its Permian Basin production volume would more than double to 1.3 million bpd as a result of the deal. XOM is expecting this number to increase to 2 million bpd in 2027. Hypothetically, if the deal closes in the middle of 2024 and the 2 million bpd number is reached in 2027, XOM will increase its Permian production by 53.85% over a 3-year period. The Energy Information Agency recently delivered its Annual Energy Outlook update and provided some critical information on the future of energy in the United States. The EIA has provided many different scenarios, and in most cases, oil and gas will expand from their 2022 levels through 2050 on a total installed generating capacity basis.

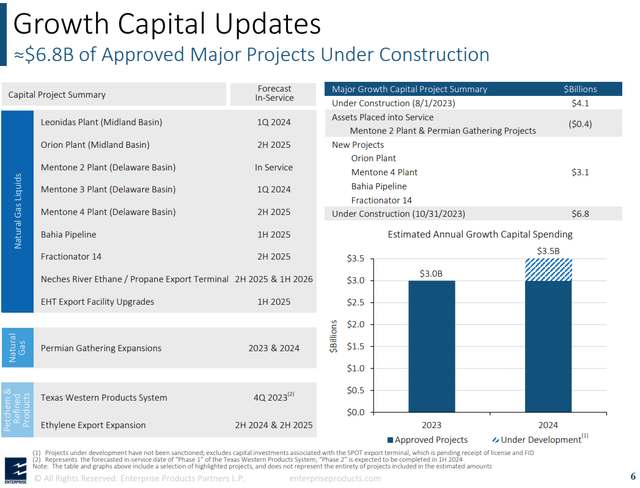

All roads lead to an increased amount of energy needed both domestically and internationally. The EIA is projecting that production for oil & gas will continue to increase as the decades pass, and XOM is the latest company to make a splash in the Permian. No matter which basin we’re discussing, when production increases, so does the need for takeaway capacity. EPD believes that oil production in the Permian Basin is on track to increase by more than 700,000 bpd in 2023 and that total production could reach 7.5 million bpd by the end of 2030. EPD is one of the premier midstream operators, and they are strategically building new takeaway capacity for the energy industry, where the most growth is projected to occur. This will cause current partners to expand their contracted takeaway capacity with EPD and should allow EPD to grow its DCF for years to come.

EIA

Enterprise Products Partners delivered a solid Q3 despite the fluctuation in EPS

EPD was down yesterday on earnings, but I think Mr. Market is looking at the wrong metrics. Midstream operators generate large amounts of cash that are distributed to unitholders, and the retained DCF is reinvested into the business. In Q3, EPD generated $1.9 billion in DCF and declared a distribution of $0.50 per unit for Q3. EPD is operating at a 1.7x distribution coverage ratio and retained $773 million from Q3’s DCF after the distributions were accounted for. EPD’s adjusted cash flow provided by operating activities (AFFO) was $2.0 billion in Q3, and its payout ratio, which includes distributions and buybacks, was 56% of its AFFO and 90% of the adjusted free cash flow (AFCF). On a trailing twelve-month basis (TTM), EPD has generated $48.74 billion in revenue, $5.5 billion in net income, $7.47 billion in non-GAAP DCF, and $9.2 billion in non-GAAP Adjusted EBITDA.

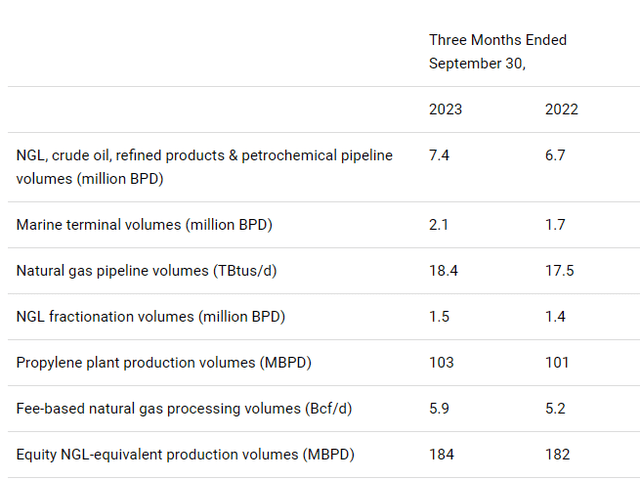

On an operational basis, despite a challenging environment with record heat in August and September that impacted EPD’s processing plants throughput and refrigeration of their NGL export facilities, they transported 12.2 million barrels per day of crude oil equivalent. EPD’s transported and production metrics have increased YoY as more projects have been put into production. There were some significant announcements in the Q3 report that are bullish for EPD’s future.

Enterprise Products Partners

EPD announced that it will expand its natural gas liquids (NGL) business by building 2 additional 300 million cubic feet today processing plants in the Permian, bringing their processing trains in the Permian to 19. EPD will convert its 210,000 bpd Seminole crude oil pipeline back to NGL service to support needed Permian NGL takeaway capacity. EPD also announced the Bahia 30-inch NGL pipeline that will originate in the Permian and deliver up to 600,000 barrels a day of NGL into its storage system in Chambers County. EPD will be able to switch services between crude and NGLs with the Seminole pipeline due to the expansion of EPD’s new TW refined product system. EPD’s expanded backlog of projects should allow them to continue generating increased levels of DCF, which should pave the way for distribution increases.

Enterprise Products Partners

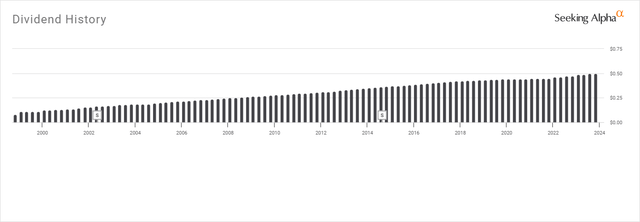

Not many companies can increase their distributions or dividends for 25 consecutive years, and EPD is currently in a very selective group. EPD recently increased its annualized distribution to $2 per unit and currently yields 7.56%. With a 25-year record of consecutive distribution increases, a 7.56% yield, and a 2.92% 5-year average growth rate, EPD is a strong income investment. We’re headed toward the end of a Fed-tightening cycle, and the demand for energy continues to grow with no path leading away from traditional fossil fuels. We’re getting the Fed decision this week, followed by another speech from Jerome Powell. All signs lead to a pivot sometime in 2024, and as the risk-free rate of return starts to decline high-yield investments could come back into favor. I think EPD is in a prime position to keep delivering on its growth initiatives while increasing the distribution, and when the Fed cuts, EPD could become a proxy for maturing risk-free assets.

On the earnings call, management indicated that expanding in the Permian will provide direct and indirect opportunities for its crude and natural gas businesses. While adding to its previous growth capital backlog, EPD specifically stated that they do not expect the additional capital investments to impact the distribution’s future growth or buyback activity in 2024. While some may look at this quarter as a mixed bag, EPD generated $1.7 billion in DCF and continues to be a cash-generating machine for its investors. The future growth should correlate to future distribution increases, and there is no reason why EPD won’t hit the 3-decade mark for annualized dividend increases in my view.

Seeking Alpha

Conclusion

This was an exciting quarter for long-term investors as EPD added to its backlog of projects. XOM made a statement acquiring PXD and sees their Permian production increasing by over 50% in 2027. EPD is one of the largest midstream operators and is following the money by adding needed capacity to facilitate the additional production that will occur in the Permian. EPD has traded basically flat over the past 5-years and continued to grow its distribution. I think that if you’re looking for income, EPD is one of the best companies to add, as their distribution history speaks for itself. I also feel that units of EPD could turn the corner in the coming years as energy production increases and upstream producers look to companies such as EPD to move the additional capacity. Please don’t forget that EPD issues a K-1 tax package, so if you’re going to add units, please look at the tax implications.

Read the full article here