Investment Thesis

UiPath (NYSE:PATH), the world’s leading robotic process automation (RPA) company, is helping humanity free itself from dull, repetitive tasks. RPA is the fastest-growing global enterprise software market, and it’s easy to see why. RPA robots can handle a wide range of tasks, from processing invoices and sales notes to reading contracts and holding conversations. This frees up human workers to focus on more complex and creative tasks.

UiPath’s vision for RPA is to have robots and AI complete routine tasks, while humans handle the exceptions. This would allow businesses to operate more efficiently and effectively, and it would also give workers more opportunities to develop their skills and knowledge.

UiPath Overview (PATH Investor Relations)

Estimates suggest that 85% of large organizations and enterprises will use some form of RPA in the coming years. Businesses want robots to automate as many processes as possible. RPA can save businesses money, increase staff productivity, create a better work environment, and help retain high-quality employees. UiPath has the ability to offer the tools and technology to make all of this possible, and it’s just a matter of time before we see widespread adoption.

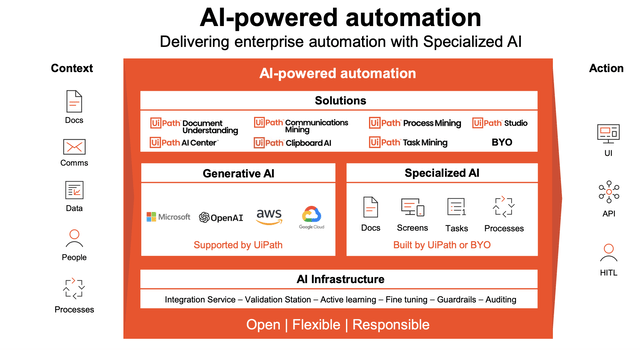

UiPath has seen wide adoption of its product offerings in recent years. Sales grew 18.8% in the company’s last fiscal year (FY), and analysts expect continued high teens and low 20% sales growth in the coming years. This is due to the global adoption of AI and RPA. Estimates suggest that the industry will continue to grow rapidly, with a compounded annual growth rate (CAGR) of 38.2% to approach $31 billion by 2030. I personally believe that the industry will be much larger than that by 2030, given the power of generative AI and the fact that autonomous vehicles are just around the corner. Below are just a few examples of what UiPath’s products can offer customers. This is just the beginning of what they can do.

UiPath AI & RPA Offerings (PATH Investor Relations)

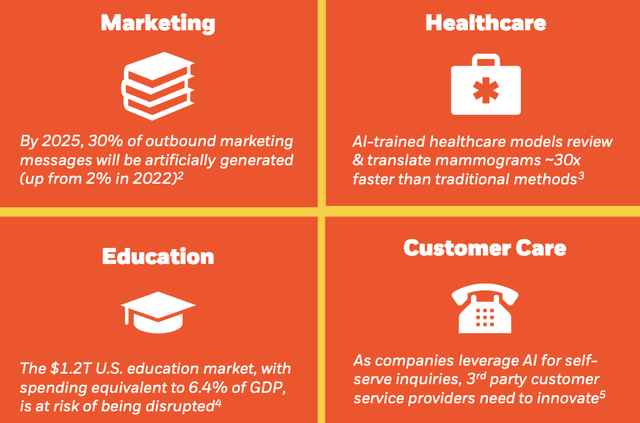

The last and most important part that I want to note, which makes me bullish on not just UiPath but on AI, RPA, and the industry as a whole, is the impact it can have on companies’ operating margins. Cathie Wood’s Ark Invest published a research article, “Automation Could Double Operating Margins and Equity Markets by 2025,” in which they dive into the numbers of production and efficiency of AI/RPA. The great thing about UiPath’s services is that they are not tailored to one service or industry. UiPath can help every kind of business be more efficient, productive, and profitable. Below are just a few examples of how UiPath will impact different industries.

AI & RPA Industry Impacts (Black Rock Research)

Overall, I think UiPath is a great way to play the AI and robotic process automation expansion catalyst. The company is a leader in the industry and has the advantage of being an early player in the technology. UiPath’s quickly growing annualized recurring revenue (ARR) proves that the adoption of its products is real. CIOs across the world will be looking to use UiPath’s offerings to help companies hit their production and profitability goals quickly and efficiently.

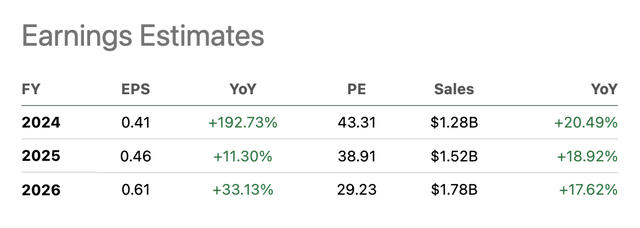

UiPath has been improving its own fundamentals quickly, focusing on profitable growth. Non-GAAP operating income (loss) went from -$11.2 million in Q2 last year to $30.1 million this year. For risk-averse investors, UiPath may not be the best choice, as it is trading at a price-to-earnings (P/E) ratio of 42.3. However, for growth investors willing to take on risk, UiPath is a good option, given its high analyst-expected growth rates over the coming years. UiPath is expected to grow into its valuation and ultimately does not look too expensive on a forward valuation basis.

UiPath Analyst Estimates (Seeking Alpha)

I suggest gradually building a position in UiPath over time. Watch quarterly earnings reports closely for changes and adoption trends. Buy the dips and pullbacks. UiPath has generational technologies that will transform the working world. This is an opportunity you won’t want to miss.

Breaking Down the Financials

Starting at the top, UiPath’s non-GAAP gross profit margins increased from 84% in the prior year’s Q2 to 86% in the most recent quarter. This means that the cost of revenues has been decreasing as the company scales and becomes more efficient. UiPath’s gross margins are also well above the sector median, which is just above 48%. High gross margins will eventually show up on the bottom line once the company is out of its growth phase.

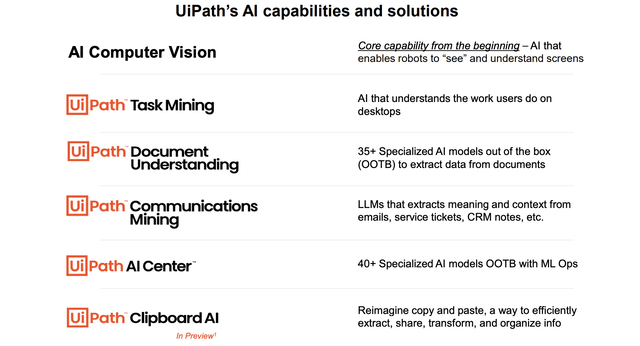

In UiPath’s last annual report and Q2 earnings release, we saw a common trend: the company spent less on sales and marketing and increased research and development (R&D) expense. UiPath’s products and capabilities are starting to build a reputation for themselves as a leader in RPA, so the company is able to spend less on marketing and still grow sales. UiPath is increasing its R&D to stay ahead of competitors’ technology and ensure that it always has the leading edge tech offerings.

UiPath Tech Offerings (PATH Investor Relations)

UiPath has been investing in its future, while also efficiently cutting costs to improve profitability. Last year, the company produced non-GAAP EPS of $0.14. This year, analysts expect that to nearly triple to $0.41. UiPath is growing, and knowing economies of scale, margins, and profitability will only get better as their products speak for themselves.

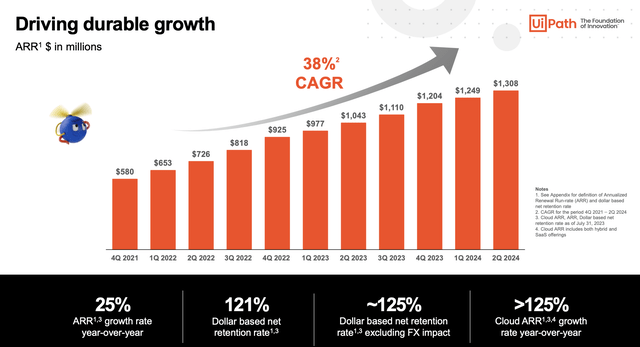

What intrigues me about UiPath, along with its products and industry, is its clean balance sheet. UiPath has no long-term debt and only $63 million in total debt. It has $1.09 billion in cash on hand, and if you include cash equivalents and short-term debt, it’s $1.8 billion. Liquidity or excessive debt is not a problem, which is great for a company still in its growth phase. Its assets-to-liabilities ratio is 3.8x, showing the true strength of its balance sheet and financial condition. UiPath is in a great place to continue growing and is ready for a downturn or change in economic conditions. ARR continues to improve, and as UiPath brings in more clients, its profits and cash pile will only continue to increase.

UiPath ARR Growth (PATH Investor relations)

Non-GAAP adjusted free cash flow (FCF) for Q2 came in at $46.6 million, up from negative FCF in the previous quarter of -$23.3 million. Currently, FCF sits at $167.9 million, which is up from -$33.8 million last fiscal year. UiPath currently has an FCF yield of just under 2%, which is not amazing but solid for a tech growth company that has not even been public for 3 full years.

UiPath has produced positive cash from operations (CFO) for three consecutive quarters now, and I expect that trend to continue. Its cash on hand has slowly been decreasing over the past few years, but I expect its cash pile to reaccelerate in the coming years. With virtually no debt and growing popularity and usage, I believe UiPath is positioned for high growth and stock price appreciation in the coming years.

My Price Targets

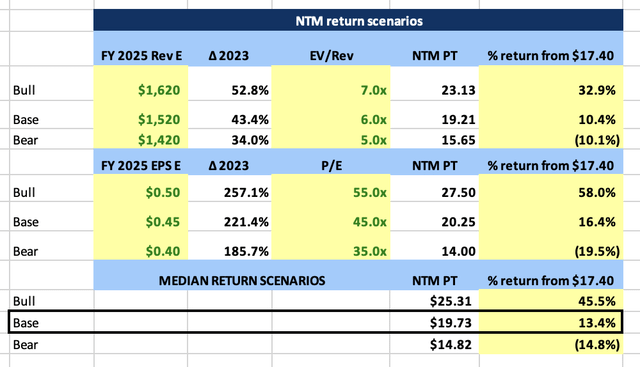

I have calculated my price target for UiPath, using current analyst estimates and valuations. My short-term price target for the next twelve months (NTM) is $19.73, which would represent a 13.5% upside from our current price of $17.4. PATH is currently up over 41% year-to-date (YTD), which has lowered the favorability of the risk-to-reward ratio (R:R). My calculations show that at current prices, the R:R is 3.1x, which is what we like to see (greater than 3x). However, the R:R was in the double digits at the start of the year. As the stock continues to drop, the more appealing the price becomes. My price target high for the stock in the NTM is $25.31, which would be a 45% move from current prices, with a low of $14.82, a 14.8% downside risk.

UiPath NTM Price Target Scenarios (Author Calculations Based on Analyst Estimates From Data on Koyfin)

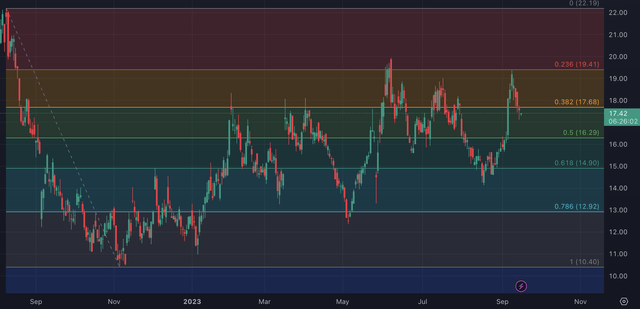

Looking at the technicals and using the Fibonacci retracement tool, we can see that the stock bounced off resistance at $19.41 and has since pulled back. The stock has dropped straight through the .382 level, and $17.68 is now the level to watch. What was support is now resistance, and it will be a key price to watch for the stock. A clean break through of that level could mean the stock is headed back to $19+. If the stock can’t break $17.68, it may be heading back down to the $16s.

PATH Stock Price Chart (Trading View)

Long term, I see a lot more upside to PATH over time. Sales will continue to increase as worldwide adoption trends change. Profitability will also continue to improve, as this is on the front of management’s agenda. However, I do not believe that forecasting and using a discounted cash flow analysis would be very accurate or reliable. PATH is still finding its way to steady profitability, and it is difficult to tell where its operating margins will settle in. It is also difficult to predict sales growth accurately. Analyst estimates currently range from 18% to 20% for the next three years, but if RPA and AI are as big as everyone seems to think, sales could reaccelerate as we have technological breakthroughs.

Risk

The first risk I want to bring to your attention is share dilution. As I mentioned before, the company does not have a lot of debt. However, it seems like the company has been taking advantage of a high stock price and extended valuation by offering new shares to raise equity and cash. Since June 2021, shares outstanding have increased 11%, from 508.8 million shares to 566.7 million shares. If you own UiPath, depending on when you bought in, you may have seen share dilution and price depreciation. With interest rates high, I doubt UiPath management will take on much debt until they come down. That being said, if they continue to expand and use up cash, offering more shares could be on the table. This is something to watch going forward.

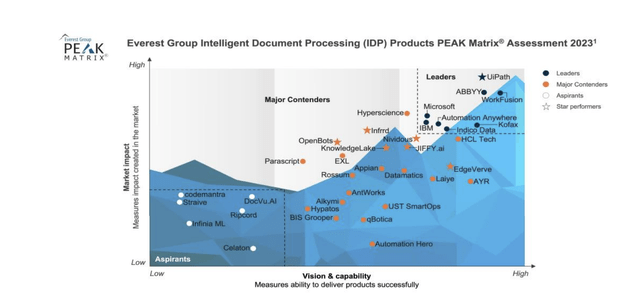

The second risk to note is the wide range of competition and the impact it could have on the company. UiPath is competing with not only other startups and unicorn companies with leading-edge technology, but also tech powerhouses like Google (GOOGL), Microsoft (MSFT), and Meta. These companies have more money, more resources, and more power to try to get the job done. It is crucial that UiPath continues to innovate and offer the best products and automation possible, or they will start to lose market share. A competitive and crowded industry can also drive down margins as companies try to competitively price services against one another.

UiPath Competitive Landscape (PATH investor Relations)

The last risk I want to note is not a company problem, but a stock price concern: the high P/E valuation. At 42x this year’s earnings expectations, you can say that UiPath is overvalued or overextended. However, I see 42x as justifiable if UiPath can actually execute and see high teens or low 20% sales and earnings per share (EPS) growth in the coming years. If management were to come out and cut estimated growth rates, the stock could be hit hard and see a drop back to its 52-week lows at $10.40, which occurred in November 2022. The sector median P/E is around 22x, which means that if UiPath traded at that 22x with $0.41 EPS expected, that would be just over $9 a share. However, I believe that UiPath will see sales reaccelerate in the coming years as AI and RPA become more widely adopted. That is why P/E and management’s outlook will be key to valuing and predicting the direction of the stock price.

Conclusion

UiPath is in the right industry at the right time. AI and process automation are at the forefront of the minds of inventors and businesses. The capabilities are endless, and the impact on businesses and the economy will be profound. UiPath’s products and services allow businesses to produce more, make more, and do more, all while satisfying customers. The company is growing rapidly and retaining more and more customers each year.

People get tired of doing boring old jobs because we are not meant to do repetitive, tedious work. UiPath uses AI tools and robotic process automation to allow technology to do these tasks for us. People can handle the one-offs, but robots can do the dirty, nitty-gritty work. Plus, they can work 24/7/365, minus any time for maintenance. This will allow companies to drastically boost production and profitability, two goals that every company has.

The potential for the industry and UiPath, an industry leader, is exponential. This stock is not for everyone—the risks are real, and the valuation could be extended, depending on how you see it and value the company’s expected growth rates. Overall, I believe that slowly building a position in the stock is a great strategy for long-term growth investors. Soon enough, everyone in the world will be using some form of UiPath’s products. You don’t want to be left behind. Technology is a great thing that is always evolving. We have to adapt as time goes on and mankind’s knowledge and power grows.

Read the full article here