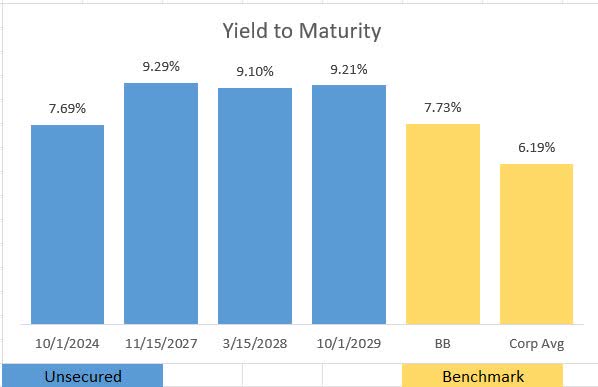

Brandywine Realty Trust (NYSE:BDN) is a real estate investment trust that owns a diversified portfolio of assets. The company has a BB credit rating, but three issues of its corporate debt are trading at a significantly higher yield than its peers. The 2027 maturing debt is yielding 9.3% to maturity and represents an attractive fixed income security for investors.

FINRA

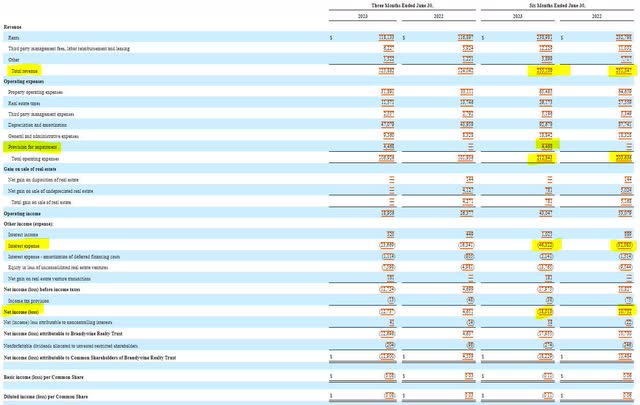

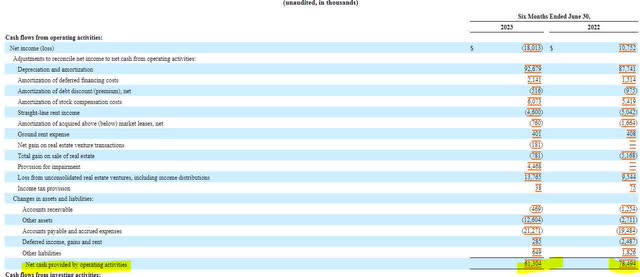

Brandywine’s profitability for the first half of this year has slipped compared to the same period last year. Revenue increased by a modest $4 million compared to a year ago while operating expenses were $9 million highly, but half of that variance was due to impairment costs. Interest expenses increased by $14 million, which shifted the company’s net income from 2022 to a net loss for the first half of 2023.

SEC 10-Q

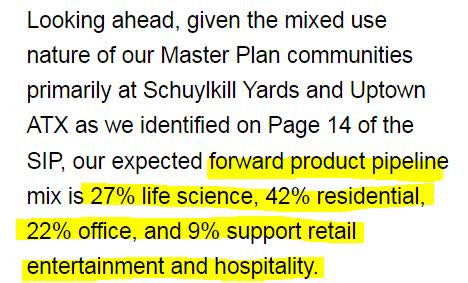

While investors may be concerned about Brandywine’s investment in office properties, it’s important to note that only 22% of the company’s portfolio is in the office space. The company has larger investments in both life sciences and residential. Despite the presence of offices in the portfolio, occupancy remained stable at 89% from last year to this year.

Earnings Release SEC 10-Q

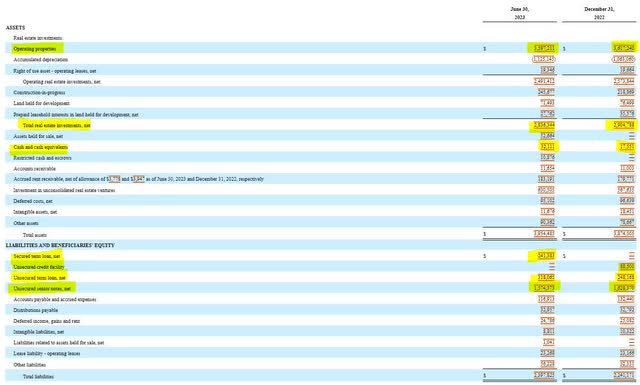

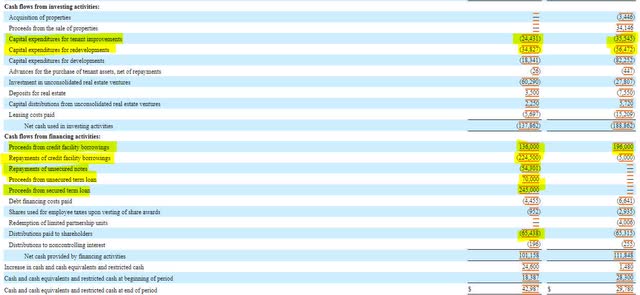

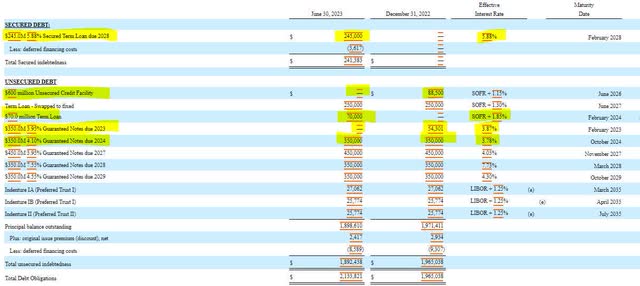

Brandywine’s balance sheet shows the shifting in debt that the company has taken during 2023. The company paid off its credit facility and paid down some of its senior notes, but it came at the expense of a larger secured term loan and increasing the balance of its unsecured term loans. Interest bearing debt has increased from just under $2 billion at the beginning of the year to $2.13 billion at the end of June.

SEC 10-Q

The cash flow statement provides more detail as to why the company needed to borrow additional funds during the first half of this year. Operating cash flow declined, mainly due to the increased interest expense, and while the company is still free cash flow positive after capital expenditures, the company had an investment commitment to a joint venture and dividends to shareholders which created the need for additional financing. While the company did reduce its dividend recently, cash flow pressures may force it to reduce the dividend further in future quarters.

SEC 10-Q SEC 10-Q

While I don’t believe that restructuring is in Brandywine’s future, I believe the 2027 notes are the best bet amongst the fixed income options because they offer the highest current return, and the company has a $70 million term loan and $350 million in unsecured notes maturing in front of the 2027 next year. The company has an untapped $600 million credit facility along with cash on hand that could easily absorb these maturities.

SEC 10-Q

Brandywine does face interest rate risks should rates continue to rise. The company has $400 million in variable interest debt in addition to the $350 million notes (which currently pay 4.1% interest) coming due next year. Higher interest expenses could further erode cash flow and force further dividend reductions. Additionally, material losses in office, residential, or life science occupancy could hurt revenue and create additional financial challenges.

Brandywine’s cash flow is stable enough to support its near-term debt maturities. The company has a diversified portfolio that has provided stable occupancy and positive free cash flow. The company’s dividend is in danger as it is not covered by free cash flow, but the unsecured bonds provide income no matter what the dividend policy is.

Read the full article here