Investment thesis

Tesla, Inc. (NASDAQ:TSLA) electric vehicle (“EV”) Q3 deliveries exceeded our expectations of 420 thousand EVs and totaled 435 thousand EVs, despite plant shutdowns for production upgrades. Continued price cuts did not result in a critical decline in the company’s margins during Q3, which were also better than we expected. Tesla delighted its customers with the long-awaited news of the start of pilot production of the Cybertruck and ambitious plans for mass production of 250 thousand EVs by 2025. R&D expenses continued to rise due to the cost of building Cybertruck prototypes and testing pilot production, combined with spending on AI technologies such as Optimus and Dojo. Tesla, Inc. continues to invest through positive cash flow from operations. Rating is hold.

The outcome of the price war

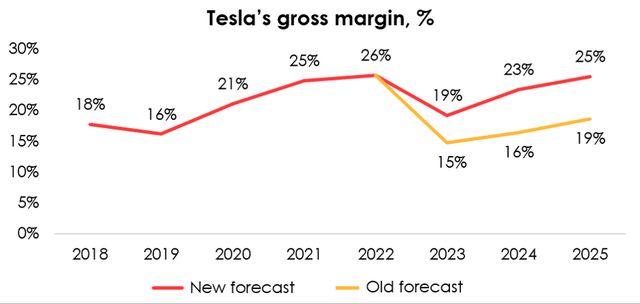

As we wrote in January 2023, Tesla started making massive price cuts for all of its electric vehicle models. Naturally, such an extended period of reduced prices could not but affect the company’s financial results, although there was also a positive effect last quarter. In 2Q 2023, Tesla set a sales record of 466 thousand EVs, which, combined with falling prices for the materials used to make lithium-ion batteries, led to record revenue of almost $25 bln and gross margin of 18.2% (-1.2 pp q/q).

Despite the scheduled shutdowns of Tesla’s plants for upgrades, EV sales were better than we expected. In 3Q 2023, the company sold 435 thousand EVs with a margin of 17.9% (-3 pp q/q), which was partially offset by the continued decline in the prices of raw materials. Importantly, Tesla makes sure that, when it reduces the production cost of its electric cars, it doesn’t sacrifice the quality of the final product, which is accomplished by relying on its own resources where possible (for example, the company builds its own batteries and makes proprietary Dojo supercomputers). Over the past four quarters, the company has succeeded in reducing production costs, and declining prices of key raw materials have only helped: In 3Q 2023, the average cost of producing one electric car was $37.5 thousand, down from $37.9 thousand in 2Q 2023, of which about a quarter is the cost of producing its own lithium-ion battery.

We expect the company’s average annual margins to recover on the back of lower production costs, and after it receives approval to introduce the full self-driving (“FSD”) autopilot and brings its take rate to 15% by 2025.

Invest Heroes

Outlook for EV production

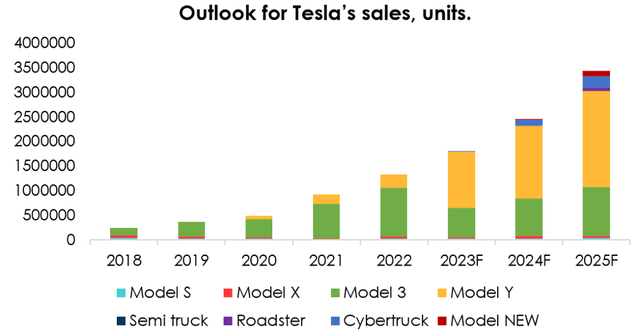

Along with the financial results for 3Q 2023, Tesla has announced the start date of Cybertruck sales – November 30, 2023 – and gave long-awaited comments regarding production. It has been reported that, in addition to the production of prototypes, the company has started pilot production at a plant in Texas with a capacity of more than 125 thousand units, which is set to gradually expand to 250 thousand units, but not before 2025. CEO Elon Musk underscored how unique the Cybertruck model is, saying that makes Tesla incur higher costs for its production, compared with the models that were released before. Therefore, despite the huge demand (more than 1 mln people have booked Cybertrucks), there are some difficulties to overcome before the start of their mass production, and, therefore, before securing any positive cash flows from the effort in the next 12-18 months.

We are maintaining our previous forecast for Cybertruck sales at 2 thousand units for 2023 and 117.5 thousand units for 2024. Due to the lack of official news regarding the start of deliveries of other previously announced but yet unreleased models, such as Semi Truck and Roadster, we are maintaining our forecast that their sales will start in 4Q 2024.

The company still plans to produce 1.8 mln electric vehicles in 2023, despite the reduced output in 3Q 2023. This means Tesla will have to sell a record 475.9 thousand EVs. We believe this number is realistic and are forecasting it will be even bigger, 482.1 thousand EVs, given the company’s commitment to ratchet up Model Y sales every quarter and the sales growth rate that we are projecting.

We expect the Model Y to continue to be Tesla’s flagship vehicle in terms of deliveries. However, due to lower sales in 3Q 2023, which produced a low-base effect, and the expected rate of sales growth in 2024, we have lowered our sales forecast for both Model 3/Y and Model S/X. Thus, we expect Tesla to sell 1.8 mln EVs in 2023 and 2.45 mln EVs in 2024, of which 1.7 mln and 2.2 mln, respectively, will be Model 3/Y.

Invest Heroes

Tesla sold 435 thousand EVs in 3Q 2023, down from the record sales of 466 thousand EVs in the previous quarter, but up from our forecast of 420 thousand EVs. We are lowering our forecast for EV sales from 1.86 mln to 1.81 mln EVs for 2023 and from 2.9 mln to 2.45 mln EVs for 2024 due to a slight decrease in the forecast for Model S/X sales, by an average of 3-5 thousand every year, and – much more importantly in terms of how much that contributes to Tesla’s revenue and the total number of EV sales – due to a decrease in the forecast for Model 3/Y sales from 1.79 mln to 1.74 mln EVs for 2023 and from 2.69 mln to 2.24 mln EVs for 2024, on account of our reduced estimate for the growth of sales of these models, and following the less-than-expected sales in 3Q 2023, which produced a low-base effect for further forecasts.

Moving on from the key segment of electric vehicles, the energy segment generated a record revenue of almost $1.6 bln (+40% y/y) in 3Q 2023. Energy storage deployments made up 3,980 MWh (+90% y/y). Megapack is the main growth driver in this segment. Solar deployments declined by 26% q/q to 49 MW due to persistently high interest rates.

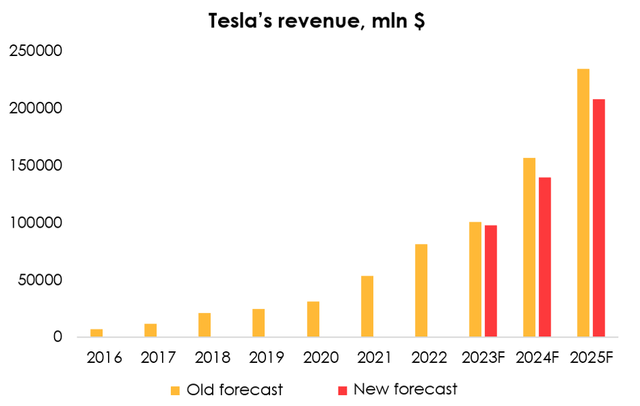

Therefore, given the reduced forecast for EV sales, and the added financial impact from the sales of the FSD option, we are lowering the forecast for Tesla’s revenue from $101 bln (+23.5% y/y) to $98 bln (+20.5% y/y) for 2023, and from $234 bln (+49.3% y/y) to $208 bln (+48.7% y/y) for 2025.

Invest Heroes

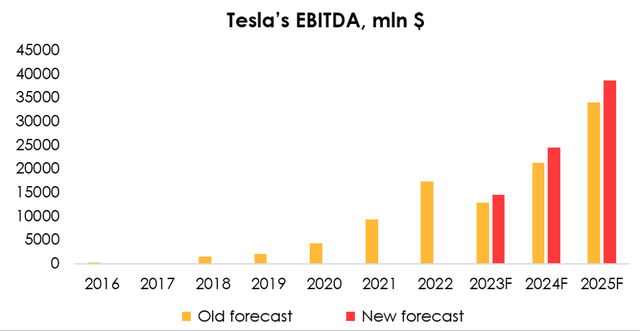

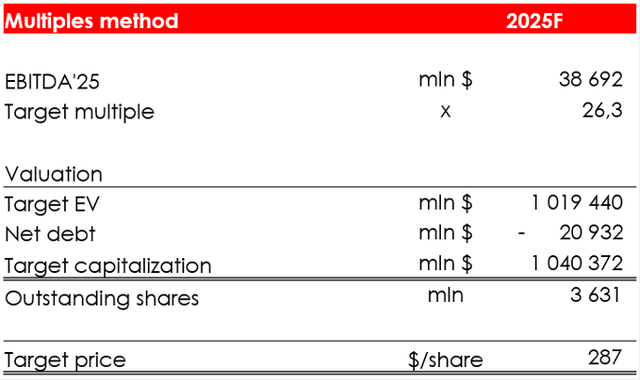

Despite reducing the revenue forecast, we are raising the forecast for Tesla’s EBITDA from $12.9 bln (-25.8%) to $14.6 bln (-16.2% y/y) for 2023, and from $34.1 bln (+60.2% y/y) to $38.7 bln (+57.8% y/y) for 2025, in a move that’s driven by the reduction of the forecast for the cost of making one EV from $39.6 thousand to $37.9 thousand for 2023, and from $41.8 thousand to $40.7 thousand for 2025.

Invest Heroes

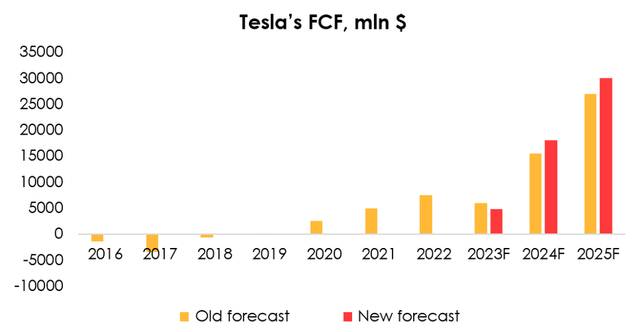

The forecast for cash flow has been reduced from $6 bln (-20.7% y/y) to $4.9 bln (-35.5% y/y) for 2023 and raised from $15.5 bln (+158.4% y/y) to $18.1 bln (+271% y/y) for 2024, and from $26.9 bln (+73.9% y/y) to $30.1 bln (+66.2% y/y) for 2025. The changes were driven by adjustments in the size of own working capital, namely an increase in the inventory turnover ratio for the next few quarters due to the trend for a rising inventory, and a decrease in the company’s accounts payable turnover ratio.

Invest Heroes

Valuation

We are raising the target price of the shares from $217 to $246 due to:

- the increased EBITDA and free cash flow (“FCF”) forecasts for 2024 and 2025;

- the increased forecast for gross margin until 2025 due to the reduction of the estimated costs to produce one EV from $39.6 thousand to $37.9 thousand for 2023, and from $41.8 thousand to $40.7 thousand for 2025;

- the shift of the FTM valuation period by 1 quarter, which means future financial results have gotten closer.

Based on the new assumptions, we are assigning a hold rating to the stock.

The share price estimate of $246 has been achieved by computing the company’s valuation based on the multiples method and discounting it at the rate of 13% per annum. Previously, we estimated the company’s value using not only the multiples method but also FCF yield. We decided to abandon the latter, as due to the large delay with the start of sales of the previously announced models, the FCF yield method significantly underestimates TSLA and differs from the multiples method several times over.

Invest Heroes

Conclusion

The company’s margin continues to be fairly high, despite reduced prices for all of Tesla’s EV models, as prices of key raw materials have remained suppressed for a long period of time, consequently reducing the cost of making EVs. In addition, we expect the company’s average annual margins to recover not only due to lower production costs but also because it will receive approval to implement FSD autopilot and increase profitability levels to 15% by 2025.

Electric vehicle deliveries continue to be strong, helping Tesla maintain its leading position in the U.S. market. In the coming quarters, the long-awaited start of production of the Cybertruck, for which demand has already reached 1 million units, will create particular interest in the company. Tesla also continues to gain valuable vehicle usage data needed to train the artificial intelligence models that underpin the autonomous driving technology on which the company is betting heavily. Tesla says that its full self-driving (FSD) technology could one day account for much of Tesla’s value and give it the cushion of safety that it lacks for competitors struggling to make their electric car operations profitable.

Read the full article here